Gifting, inheritance tax and life assurance, a simple guide for families

Correct as at June 2026. The inheritance tax allowances and thresholds referred to in this article relate to the 2026/27 UK tax year.

Many people want to pass wealth to children, grandchildren or other loved ones during their lifetime. This might be to help with a house deposit, reduce the future value of an estate, or simply allow family members to benefit sooner rather than later.

However, larger lifetime gifts can still have inheritance tax consequences if the person making the gift dies within seven years. Life assurance can play a useful role in protecting the family from an unexpected tax bill.

The seven-year rule

Most outright gifts to another individual are known as potentially exempt transfers, often shortened to PETs. This means the gift is not immediately subject to inheritance tax, but it only becomes fully exempt if the person making the gift survives for seven years. This assumes the donor does not continue to benefit from or retain enjoyment of the gifted asset after making the gift, as different rules may apply where a benefit is retained.

Gifts into some types of trust, such as discretionary trusts, are usually treated differently and may be chargeable lifetime transfers. The same broad protection principles can still apply, but the tax treatment is more complex and advice is usually essential.

Some gifts are immediately exempt from inheritance tax. Common examples include the £3,000 annual exemption, small gifts within the permitted limits, gifts between spouses or civil partners, and gifts made regularly out of surplus income where the rules are met. Gifts that do not qualify for an exemption generally remain relevant for seven years.

What happens if the donor dies within seven years?

If the person making the gift dies within seven years, the gift is brought back into the inheritance tax calculation. This does not always mean the person who received the gift has tax to pay.

The key point is that the gift may use up some or all of the donor’s nil rate band, which is £325,000 for the 2026/27 tax year. If the gift is within the nil rate band, there may be no tax directly payable on the gift itself. However, the estate may lose some or all of that nil rate band, which can increase the inheritance tax payable by the beneficiaries of the estate.

For example, if someone gives away £200,000 and dies within seven years, that gift may use £200,000 of their nil rate band. If their estate is taxable, the beneficiaries of the estate could effectively suffer an additional inheritance tax cost because less nil rate band is available on death.

What if the gift is more than the nil rate band?

If total gifts made within seven years exceed the nil rate band, inheritance tax may become payable on the excess. The person receiving the gift may then have to pay the tax on that gift.

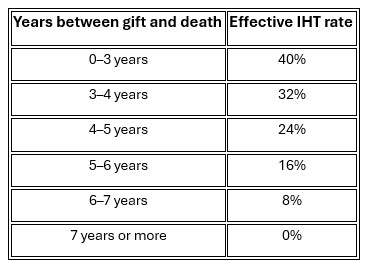

Taper relief can reduce the inheritance tax payable on gifts made more than three years before death, but it only applies where the value of gifts exceeds the nil rate band. Broadly, the inheritance tax rate on the taxable part of the gift reduces as follows:

So, if a £400,000 gift is made and the donor dies within seven years, the first £325,000 may be covered by the nil rate band, but the £75,000 excess could be taxable. If death occurs between five and six years after the gift, the effective tax rate on that excess may be 16%.

How life assurance can help

Life assurance can be used to provide money to meet a possible inheritance tax bill if the donor dies within seven years.

There are two main approaches.

1. Level term assurance

This can be used where the main risk is that a gift uses up the nil rate band and increases the tax payable by the estate. For example, if a £200,000 gift could create an additional 40% inheritance tax cost for estate beneficiaries, a seven-year term assurance policy for £80,000 could provide funds to cover that extra liability.

2. Gift inter-vivos cover

This is a special form of reducing term assurance designed to cover the tax that may be payable on a gift above the nil rate band. The cover usually starts at 40% of the taxable gift and then reduces after year three, broadly in line with taper relief.

For example, if £75,000 of a gift is potentially taxable, the maximum inheritance tax exposure is £30,000. Cover may then reduce over the seven-year period as the potential tax reduces.

Life assurance policies are subject to underwriting, policy terms and conditions, and premiums continuing to be paid throughout the policy term.

Why policies are usually written in trust

Life assurance used for inheritance tax planning is normally written in trust. This helps ensure the proceeds are paid outside the deceased’s estate and can be made available to the intended beneficiaries more quickly. Any trust arrangement should be established correctly and its suitability will depend on individual circumstances and objectives.

The key message

Gifting can be very effective, but families should understand who may bear the tax cost if the donor dies within seven years. Life assurance can provide a simple safety net, protecting both the person receiving the gift and the beneficiaries of the remaining estate. For larger gifts, trusts or more complex estates, professional advice is strongly recommended.

If you have a question about gifting, inheritance tax and life assurance, then please get in touch via the form below or call us on 01825 76 33 66.

This article is for information purposes only and does not constitute financial, tax or legal advice. Tax treatment depends on individual circumstances and may change in the future.